Fix the conveyance tax reform bill; don’t veto it

Governor Ige has included House Bill 58—the lone tax fairness proposal to make it through the legislature this year—on his intent to veto list. The governor believes that the improved economy and availability of federal relief funds means the state doesn’t need more revenue. He also noted in his rationale for veto that the bill could adversely affect affordable housing.

HB58 was advanced by the legislature to increase state revenues, and it would do that in two ways: It would temporarily dispense with general excise tax exemptions for some favored industries, and it would increase conveyance taxes on high-cost home sales by:

Doubling the tax from 70 cents to $1.40 per hundred dollars on houses sold for between $4 and $6 million;

Tripling the tax from 90 cents to $2.70 per hundred dollars on houses sold for between $6 and $10 million; and

Quadrupling the tax from $1 to $4 per hundred dollars for houses sold for more than $10 million.

(Importantly, HB58 did not change the conveyance tax rate for houses sold for less than $4 million.)

Hawaiʻi still needs the revenue HB58 would raise. Because the bill is targeted at luxury property, its tax will fall on the wealthy and not the working class, increasing equity within our tax system. And because the tax is applied on the sale of property, the bill has the added benefit of modestly discouraging real estate speculation.

Home purchase records over the past year reveal that a majority of the buyers of houses that cost $4 million or more are not full-time occupant-owners. In the current housing market, wealthy people from all over the world are buying up Hawaiʻi’s limited stock of homes and, often, leaving them empty. This drives up prices for local residents and reduces the inventory of available housing. Since our low county property tax rates encourage investors to purchase local housing for future profits or part-time vacation use, this is one of the few ways we could impose a tax on wealth.

There is, however, a flaw in the bill—but one that could be easily addressed with an amendment that could be proposed in the upcoming legislative special session beginning July 6, 2021. As written, low-income multi-unit housing developments could be subject to the increased tax rates. To guard against this unintended consequence, the legislature could simply exempt low-income housing projects from conveyance taxes.

While the economy is regaining some of its strength, and while federal relief payments have made it unnecessary to cut state programs, our policymakers need to adopt a longer view in assessing what our state will need to meet changing needs and to be resilient in the face of future challenges.

Here are some of the conditions that demand thoughtful consideration of our budget and tax systems:

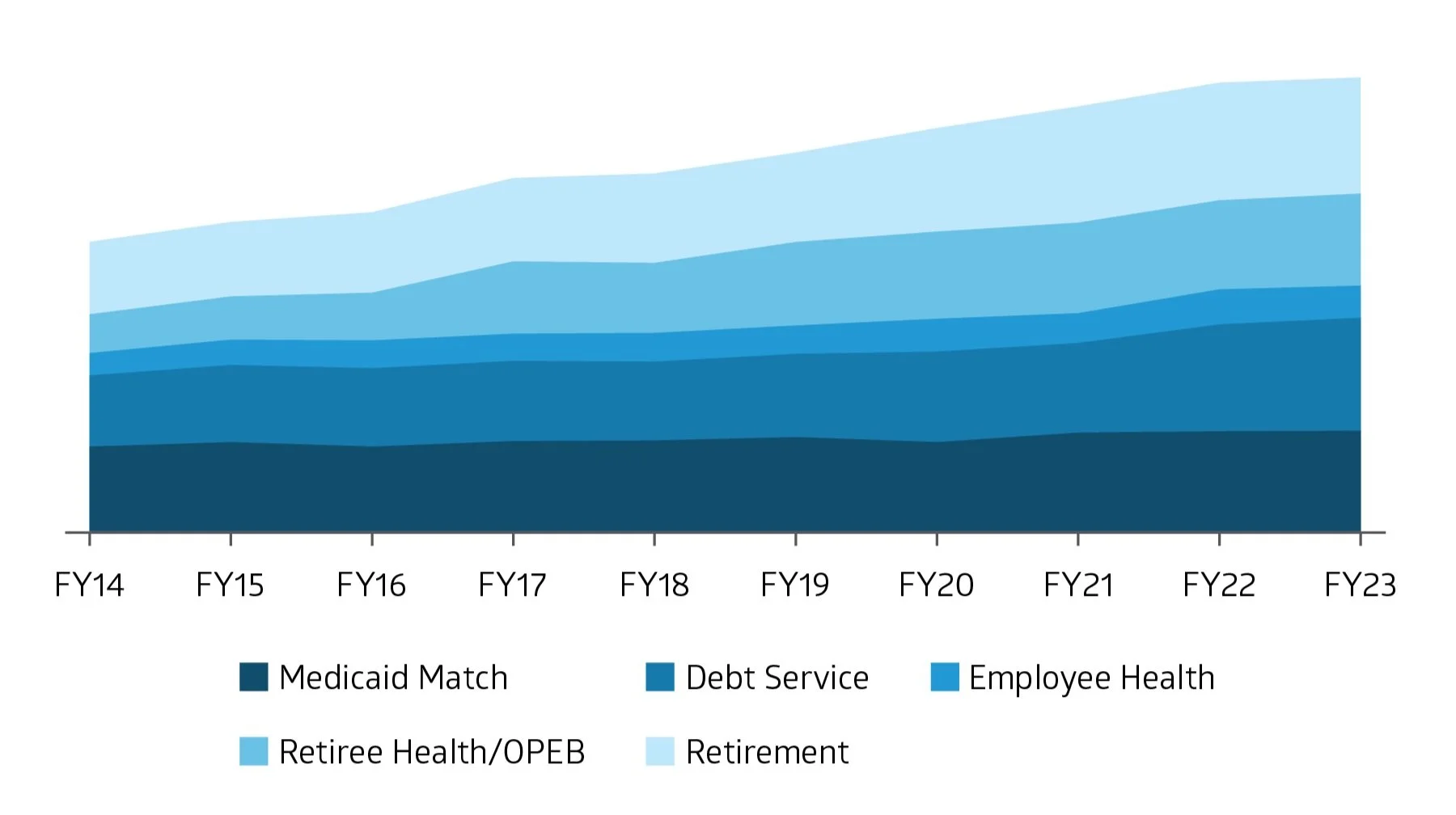

Our obligated costs (sometimes referred to as “fixed costs”) consume about a quarter of the state’s operating budget. While the state’s operating budget (in 2020 dollars) has grown by 17 percent since 2014, obligated costs have increased by 38 percent.

Figure 1. Budget for Obligated Costs, 2014–2023

Figure 1. The increase in the state’s obligations to pay for public worker retirement costs, current worker health benefits, interest on borrowing, and the state’s share of Medicaid costs. In 2014, the total, adjusted to 2020 dollars, amounted to $3.2 billion, while the current budgeted amount is $4.4 billion.

A growing proportion of our population is retiring. They pay less in taxes, both because retirees typically earn less income and because age exemptions reduce their taxable income. Hawaiʻi also fully exempts pension and Social Security income from state income taxes. This untaxed income amounted to $4.8 billion in 2018.

Figure 2. Income Tax Returns and Exemptions, 2012–2018

Figure 2. Between 2012 and 2018, the number of all residents filing income tax returns increased by 11 percent. In comparison, the returns filed with at least one age exemption (filer or spouse was 65 or older) increased by 24 percent, and the exempted income for pensions and Social Security grew by 30 percent. This trend puts increasing pressure on the proportionately shrinking working-age taxpayers.

Hawaiʻi’s low wages mean that most taxpayers pay little income tax. It is appropriate that people with limited incomes should pay lower taxes. The problem is that Hawaiʻi has a relatively small number of high income earners in our tax base.

Figure 3. Tax Returns by Income vs Tax Revenue by Income, 2018

Figure 3. 56 percent of resident taxpayers had less than $50,000 in adjusted gross income (AGI) in 2018. That majority of taxpayers contributed just 12 percent of tax revenues in 2018. Only one in five residents reported six-figure AGI, but they accounted for nearly two-thirds of all taxes owed.

Besides these concerns, Hawaiʻi needs to attend to the shortage of affordable housing, neglected infrastructure, rising seas and climate change, and invest in better pre-K through college education so our kids have a better future. While increased economic activity and federal relief funds will get us through the next year or two, policymakers need to think about longterm needs for our communities and how we’ll get the resources to pay for them.